Market Overview: Key Data and Trends

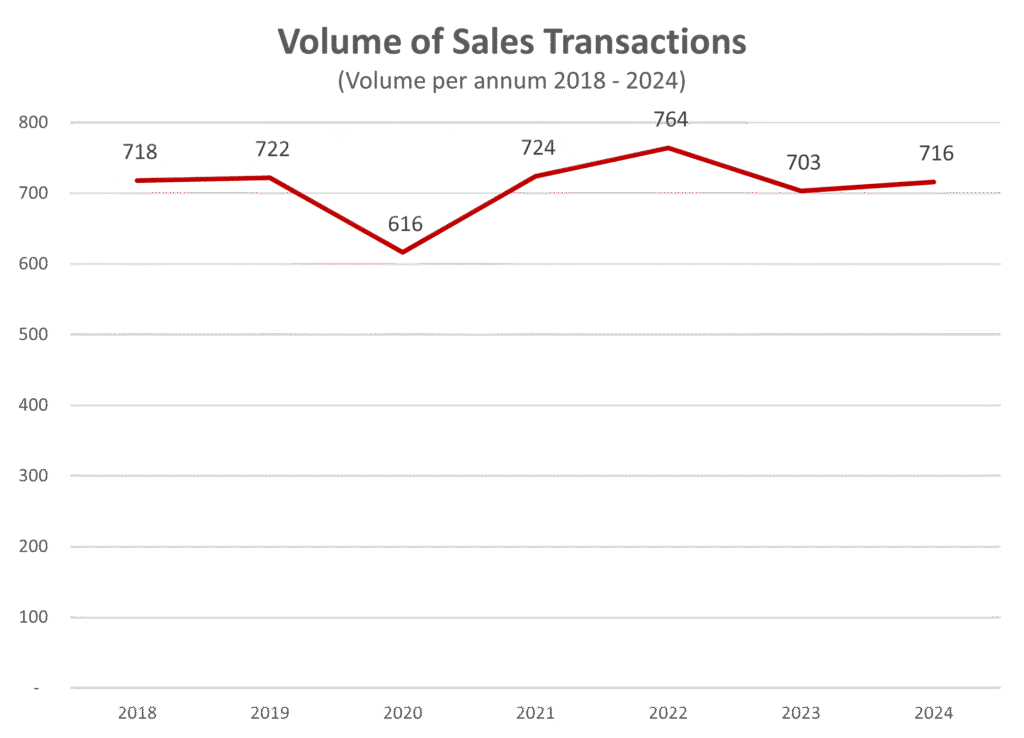

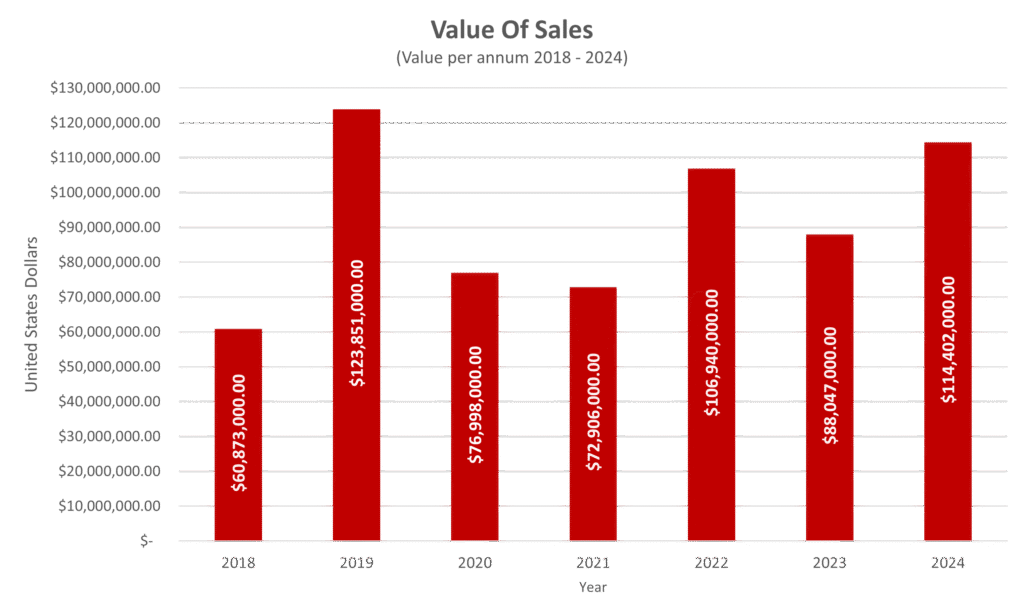

Grenada’s real estate market experienced notable growth in 2024, marked by a 30% increase in the total value of sales and a 2% rise in transaction volume compared to 2023. A total of 716 transactions were recorded, amounting to approximately USD $114.4 million.

Included in the data set: Several high-value transactions, primarily involving large development sites, have been noted on an annual basis. These transactions are significantly higher in value thereby increasing the overall performance of any given year. In some cases, the sale of one development site can be greater in value than the combined value of all other transactions for that year. The acquisition of many of these sites has been for the development of projects for the Citizenship by Investment (CBI) Programme.

- 2019: 4 development sites

- 2020: 4 development sites

- 2021: 4 development sites and 5 smaller sites

- 2022: 2 development sites

- 2024: 1 development site

Excluded from the data set: There are several transactions noted on an annual basis noted as real estate sales that are CBI sales, these transactions have been excluded from the data set. In some cases, these transactions relate to the sale of shares, fractional ownership, and sales with special conditions including citizenship and buyback options. In 2024, a total of fourteen CBI transactions were removed in the amount of USD $11,180,000 in value.

Transaction Stability and COVID-19 Impact

The volume of sales has remained relatively stable over the past seven years, with the exception of 2020, when the COVID-19 pandemic led to disruptions in office operations and property transactions. By 2021, transaction levels returned to historical norms, with steady increases continuing into 2024.

Sales Breakdown: Land vs. Improved Properties

In 2024, land sales dominated the market, accounting for 44% of total sales value and 74% of total transaction volume. Improved properties comprised the remaining 56% of sales value and 26% of sales volume. This represents a shift from historical trends, where land transactions typically constituted 80% of the market.

Sales by Property Classification: Residential, Commercial, and Agricultural

- 93% of total transaction volume

- 61% of total sales value

- Driven primarily by local buyers, diaspora investors, and some international participants

Commercial Sales

- 3% of total transaction volume

- 37% of total sales value

- Concentrated in St. George, where demand for retail, office, and hospitality spaces remains strong

Agricultural Sales

- 4% of total transaction volume

- 2% of total sales value

- Primarily purchased by local buyers, with a concentration in St. Andrew

Sales by Price Range

Land Sales

- Residential Land: 92% of transaction volume, 50% of total sales value

- Commercial Land: 2% of transaction volume, 47% of total sales value

- Agricultural Land: 6% of transaction volume, 3% of total sales value

Residential Land Price Segments

- Below USD $75,000: 83% of transactions (concentrated in St. George (34%) and St. Andrew (25%))

- USD $75,001 – $220,000: 15% of transactions (St. George (59%) and St. David (20%))

- Above USD $220,000: 2% of transactions (True Blue, Lance aux Épines, Egmont, Petite Calivigny, Fort Jeudy, and New Westerhall Point)

Commercial and Agricultural Land Trends

- Commercial land transactions were primarily in the USD $220,000+ range, concentrated in St. George, reflecting the high value of commercial land and commercial activity within this parish.

- Agricultural land sales have remained stable in the lower price ranges, primarily in St. Andrew.

Improved Property Sales

Residential Properties

- 26% increase in transaction volume compared to 2023

- 47% rise in sales of properties below USD $75,000, driven by an affordable housing initiative in St. David

Commercial Properties

- Steady transaction volume, but an increase in total sales value, reaching USD $19.1 million in 2024

Parish-Level Market Performance

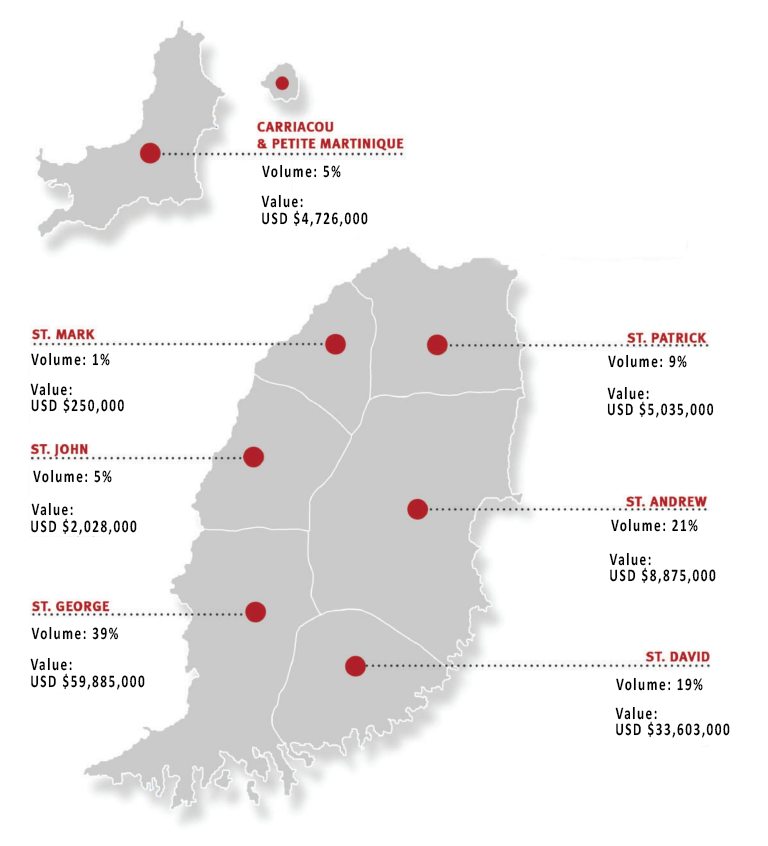

Overall market trends in the parishes remain consistent with real estate activity is concentrated in St. George, the most populous parish with high demand for residential and commercial properties.

St. Andrew continues to dominate agricultural sales, while Carriacou and Petite Martinique showed steady transaction levels up to 2024.

Future Outlook: What’s Next for Grenada’s Real Estate Market?

Looking ahead, Grenada’s real estate sector is positioned for continued expansion, influenced by local, regional and international market factors. Key emerging trends include:

- Increased condominium developments to cater to rising demand

- Growing commercial real estate investments, particularly in urban hubs

- Shifts in the education sector, affecting rental and residential markets

- Expanded affordable housing projects

- New land development initiatives

With strong local participation and ongoing investor interest, Grenada’s real estate market remains an attractive opportunity for market participants. However, external economic conditions and natural disaster impacts will play a crucial role in shaping its trajectory over the coming years.