This spring hasn’t turned out as once hoped, to say the least.

Real estate agents across the country confirmed in the most recent Intel Index survey that the rough start to spring was no aberration, and has instead extended well into April and early May.

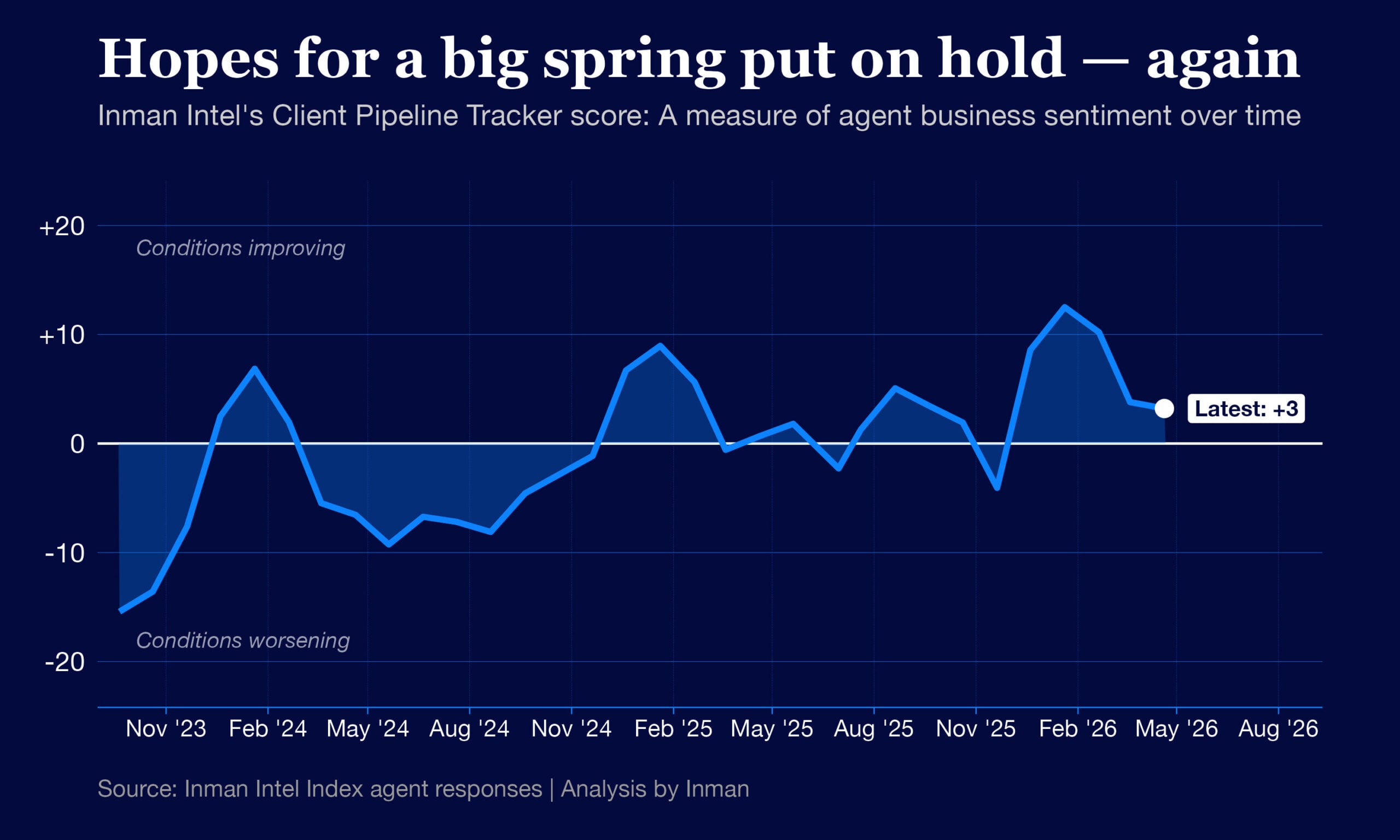

As negotiations between Iran and the U.S. over the Strait of Hormuz keep mortgage rates high, Intel’s Client Pipeline Tracker metric reached its lowest level since November, when a government shutdown temporarily spooked agents over the trajectory of the market.

While overall agent sentiment remains neutral, not negative, it’s a far cry from where it stood at the outset of the year, when a more robust recovery seemed to be in sight.

Client Pipeline Tracker score in April: +3

- Previous high point: +13 in January

- 12 months ago: +1 in April 2025

Chart by Daniel Houston

These numbers add depth and detail to a picture that has been discussed more openly among executives and financial analysts in recent weeks.

Read about the four components that went into the score — and how real estate decision-makers say they’ve adjusted their projections for 2026 — in the full report.

No bounce-back in sight

Intel’s Client Pipeline Tracker is a compilation of how agents feel about their buyer and seller pipelines — both over the past year and in the near future.

Intel described the methodology in this post, but here’s a quick refresher on how to interpret the scores.

- A score of 0 represents a neutral period in which client pipelines are neither improving nor worsening.

- A positive score reflects a market in which client pipelines have been improving, or are widely expected to improve in the next 12 months. The higher the rating, the more confident agents are that conditions are moving in a positive direction.

- A negative score suggests client pipeline conditions are worsening, or are widely expected to get worse in the year to come.

A significantly positive combined score falls around the +20 mark. This type of score would signify that much of the industry is in agreement that pipelines are improving and will continue to improve.

A significantly negative combined score, on the other hand, falls closer to -20. That’s a bit lower than where the industry stood in September 2023, the first time Intel surveyed agents about their pipelines.

For each of the four individual components that go into the score, results as high as +50 or as low as -50 are sometimes observed.

Here are the component scores from the most recent survey, and how each sentiment category changed from the previous one.

Tracker component scores

March → April

- Present buyer pipelines: -18 → -20

- Future buyer pipelines: +9 → +9

- Present seller pipelines: -6 → -5

- Future seller pipelines: +14 → +13

For the most part, the components confirm that the steep decline in agent sentiment from February to March was not a flash in the pan.

In fact, while most categories held roughly steady, present-day buyer pipeline conditions may have deteriorated further in April — with a particularly pronounced bump in agents expressing strong pessimism.

- The share of agent respondents who told Intel their pipelines had “significantly” worsened year-over-year rose from 13 percent in February to 17 percent in March. By April, this group landed at 21 percent of agents surveyed.

Optimism for the year ahead has also been notably tempered among Intel Index survey respondents.

- Agents who said they expected their buyer pipelines to grow over the next year tumbled from 49 percent in February to 36 percent in March, then settled just below 34 percent in April.

In a piece of good news for agent commissions, listing client pools appear to have remained relatively stable amid the uncertainty.

Still, agents have lowered their expectations that they’ll find as many seller clients in the year ahead as they had once hoped.

- While 50 percent of surveyed agents in February said they expected their listing pipelines to be heavier a year from now, only 41 percent said the same in March. And that share held steady in April as well, dipping slightly to 40 percent.

And these trends have been very much on the minds of real estate executives in recent public discussions with investors and financial analysts.

What executives are saying

Intel’s surveys aren’t the only signs that agent sentiment has worsened in recent months.

Zillow Group CFO Jeremy Hofmann said on an earnings call last week that a decline in revenue from market-based pricing was at least partly a result of souring agent outlooks during the first few months of the year. Transaction levels were also relatively flat.

The culprits? In January, disruptive weather events. In March and April, higher mortgage rates.

“That impacts agent sentiment when there is some excitement around the real estate industry, albeit muted, heading into the year and the transactions don’t end up occurring,” Hofmann told investors on the call.

Some of the more detailed commentary came a few weeks earlier when the homebuilder Lennar Corp. reported its earnings.

CEO Stuart Miller told investors on an earnings call in April that in addition to affordability continuing to weigh on buyers, uncertainty about the duration of the war in Iran creates a risk that consumers could see sustained higher costs associated with mortgages, gas and other consumer goods.

He also pointed to uncertainty that some Americans have over job security in the classes of work that are most disrupted by artificial intelligence.

“This uncertainty layers onto already strained household budgets and has made consumers more hesitant to commit to large purchases, particularly homes,” Miller said on the call. “Traffic has remained reasonably consistent across our communities, but the urgency to transact remains measured.”

Some executives are no longer treating this as an isolated problem that would end if, say, the Iran war were to end soon.

On Zillow’s call with investors last week, Hofmann said that declines in agent sentiment have contributed to lowered projections for the rest of the year.

“We’re just not anticipating or planning for any recovery in transaction volume throughout the course of the year,” Hofmann said.

Methodology notes: This month’s Inman Intel Index survey ran from April 22 through May 5, and received 435 responses. The entire Inman reader community was invited to participate, and a rotating, randomized selection of community members was prompted to participate by email. Users responded to a series of questions related to their self-identified corner of the real estate industry — including real estate agents, brokerage leaders, lenders and proptech entrepreneurs. Results reflect the opinions of the engaged Inman community, which may not always match those of the broader real estate industry. This survey is conducted monthly.